AI-Powered Fraud Detection for Banks: Reduce Payment Losses 40% and Enhance Team & Compliance Efficiency

Calibraint

Author

March 27, 2026

Fraud is getting harder to detect because it doesn’t look like fraud anymore, especially with the rise of synthetic identity fraud.

Powered by advances in AI development on the fraudster’s side, it blends into everyday transactions so smoothly that nothing seems unusual. Every step looks valid; every check is passed; and everything appears legitimate on the surface.

This is where AI-powered fraud detection for banks becomes the critical line of defense. A mosaic of real data points forms an identity that sails through onboarding, clears every security hurdle, and operates with a quiet, eerie legitimacy for months. By the time the mask finally slips, the vault is already empty. This leaves institutions to untangle an expensive, invisible web that was woven right under their noses.

Legacy systems, those rigid, rule-based relics of a simpler era, are drowning in this new reality. These tools are paralyzed by the complexity of modern threats. Manual reviews are too slow, and fixed rules are too brittle to catch a predator that learns and pivots in real-time. This is no longer just a technical hurdle; it is a high-stakes arms race. To survive, the industry has undergone a radical transformation, pivoting toward AI-powered fraud detection for banks to fight intelligence with intelligence.

The Real Cost Is Not What You Think

Every fraud discussion starts with the dollar figure. Mastercard research confirms that organizations lost an average of $60 million to payment fraud in the past year. That number lands hard, and it should.

But the number that rarely makes the headline is the cost of the false positive.

Compliance teams at mid-to-large banks investigate thousands of alerts each month. A significant portion flags completely legitimate transactions. The investigation still happens. The analyst hours still get consumed. The customer still experiences friction, sometimes enough to close an account. Rule-based systems were built for a different era of payment volume and a different level of sophistication. They were not designed for an environment where fraudsters automate attacks using the same generative tools that banks use to serve customers.

Mastercard’s 2025 payment fraud prevention report offers a precise picture of where the industry stands: 83 percent of industry leaders credit AI with reducing false positives and customer churn.

Forty-two percent of issuers and 26 percent of acquirers report preventing fraud attempts that would have exceeded $5 million in losses over two years. These aren’t forecasts; they represent achievements from institutions already operating AI fraud detection for banks at scale.

The question is no longer whether it works. The question is what it costs to wait.

Why Traditional Systems Are Structurally Outmatched

Rule-based fraud detection operates on a simple logic: if a transaction matches a known pattern of fraud, flag it. The problem is that fraud patterns change constantly, and updating rules requires human intervention every time.

Fraudsters know this. They test edges, find the gaps between rules, and move through them. By the time a compliance team writes a new rule, the tactic has already shifted.

Real-time payment fraud monitoring AI operates on a different principle entirely. Instead of matching transactions against a fixed set of rules, it builds a behavioral model for every account. It understands what normal looks like for each customer, each merchant category, each payment channel, and each time of day. When something deviates from that model, it flags the deviation, not the category.

This distinction matters more than it sounds.

A rule-based system sees a wire transfer and checks it against a preset threshold. An AI system does something fundamentally different. It tracks transaction amounts, locations, merchant categories, and behaviors all at once.

Spotting unusual activity, such as a sudden move to large transfers in an unfamiliar area for the customer. AI assigns a dynamic fraud score using hundreds of contextual variables, from device metadata to behavioral context, flagging fraud within 200 to 300 milliseconds of detection.

That is the operational difference between stopping fraud and reviewing it after the loss has already been settled.

Where human analysts might review hundreds of transactions per day, AI models analyze millions simultaneously without performance degradation.The math on that comparison is not subtle.

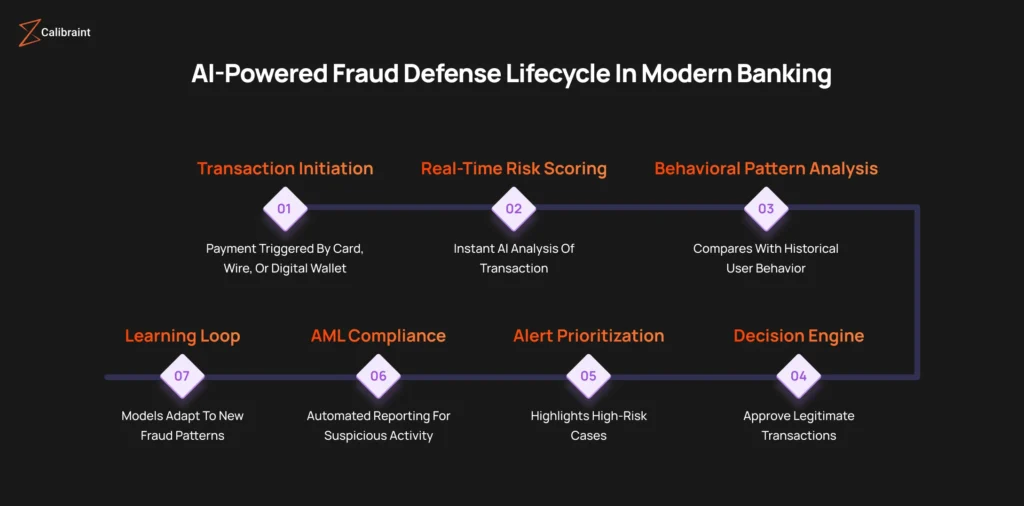

Institutions that see consistent results from AI-powered fraud detection for banks follow a structured path rather than deploying a tool and hoping for adoption.

Phase One integrates transaction data, customer behavioral profiles, and external signals into a unified data layer. The quality of this foundation determines the accuracy of everything that runs on top of it.

Phase Two trains models on historical patterns to establish behavioral baselines at the account level. This is where the system learns what normal actually looks like across retail, commercial, and digital payment lines.

Phase Three deploys real-time payment fraud monitoring AI that scores every transaction before approval. Risk scores reach the decision engine before funds move, not after.

Phase Four closes the loop. Models update continuously based on new fraud patterns, confirmed cases, and false positive feedback. The system becomes more precise over time without manual rule rewrites.

Where the Business Impact Compounds

The financial case for AI-powered fraud detection for banks is built on three layers that reinforce each other.

The first is direct fraud prevention. Real-time payment fraud monitoring AI stops losses before they occur. The savings are immediate and measurable.

The second is compliance efficiency. AI AML compliance automation for banks reduces the manual effort required for suspicious activity reporting, audit preparation, and regulatory documentation. Teams that previously spent weeks on quarterly reviews complete the same work in days. That time does not disappear; it shifts to higher-value analysis.

The third layer is the one that surprises most institutions. When you reduce false positives in bank fraud detection, customer experience improves directly. Fewer legitimate transactions get declined or delayed. Customer trust holds. Attrition from friction drops. The revenue protected is not just what fraud would have taken. It is also what poor detection accuracy was quietly costing in lost customer relationships.

AI fraud detection ROI for banking teams materializes across all three layers simultaneously. That is why the institutions that adopt early do not return to previous systems. The compounding effect is too significant to walk back.

The Strategic Moment

Fraud will not become simpler. Payment volumes will not decrease. Regulatory expectations around AML oversight will not soften.

The institutions building durable advantages right now are the ones treating AI-powered fraud detection for banks as infrastructure, not as an experiment. They are the ones whose compliance teams work on strategy because the system handles the noise. They are the ones whose customers never know how many fraud attempts were stopped on their behalf.

That invisibility is the goal. A fraud defense that works does not announce itself. It just protects, continuously, at a scale no manual process can match.

Ready to See What This Looks Like for Your Organization?

Calibraint builds AI-powered fraud detection systems designed around your payment infrastructure, your compliance requirements, and your risk thresholds.

Most institutions already have the data. What they need is a system that acts on it at the right moment.

Our team maps your current fraud exposure, identifies the gaps your existing systems leave open, and architects a solution that fits your environment without disrupting what already works.

Book a focused discovery session. Walk away with a fraud risk assessment built specifically for your institution

FAQs

1. How does AI prevent payment fraud in banks?

AI stops fraud by moving from rigid rules to real-time predictive modeling. It scans millions of data points like transaction velocity and device fingerprints in milliseconds. This allows it to spot synthetic IDs by identifying behavioral anomalies that older systems miss.

2. Can AI reduce false positives in banks?

Yes. Modern AI systems cut false positives by up to 60%. By learning a customer’s unique routine through behavioral biometrics, the system avoids blocking legitimate purchases while keeping security tight.

3. What percentage of banks use AI for fraud detection in 2026?

Approximately 90% of financial institutions have integrated AI into their fraud stacks by 2026. While global banks are fully operational, about 20% of smaller regional banks are still phasing out manual systems.

4. How does AI help banks with AML compliance automation?

AI automates AML by using smart KYC for instant verification and graph analytics to trace complex fund movements. It can also auto-draft suspicious activity reports, which reduces audit preparation time by nearly 90%.

5. What is the ROI of AI fraud detection for banking teams?

The return is massive. Top-tier institutions have generated over $1.5 billion in value. On average, banks see a 35% to 41% return on investment within two years due to reduced losses and lower operational costs.

Calibraint

Author

March 27, 2026

Let's Start A Conversation

Manage Consent

To provide the best experiences, we use technologies like cookies to store and/or access device information. Consenting to these technologies will allow us to process data such as browsing behavior or unique IDs on this site. Not consenting or withdrawing consent, may adversely affect certain features and functions.

Functional

Always active

The technical storage or access is strictly necessary for the legitimate purpose of enabling the use of a specific service explicitly requested by the subscriber or user, or for the sole purpose of carrying out the transmission of a communication over an electronic communications network.

Preferences

The technical storage or access is necessary for the legitimate purpose of storing preferences that are not requested by the subscriber or user.

Statistics

The technical storage or access that is used exclusively for statistical purposes.The technical storage or access that is used exclusively for anonymous statistical purposes. Without a subpoena, voluntary compliance on the part of your Internet Service Provider, or additional records from a third party, information stored or retrieved for this purpose alone cannot usually be used to identify you.

Marketing

The technical storage or access is required to create user profiles to send advertising, or to track the user on a website or across several websites for similar marketing purposes.