How to Build DeFi Platforms That Attract Institutional Capital: Compliance and Liquidity Lessons That Actually Matter

Calibraint

Author

April 13, 2026

Most decentralized platforms are built to be disruptive. Very few are built to be trusted. Here is the distinction between those that attract serious capital and those that remain on the sidelines of institutional finance.

The platforms haven’t changed, but the market has.

There is a version of institutional DeFi platforms that exists only in pitch decks. It is frictionless, permissionless, and infinitely liquid. It onboards sovereign wealth funds in seconds and clears billions without a compliance layer in sight.

Then there is reality.

In reality, institutional capital flows where trust is architecturally embedded, not rhetorically promised. The firms that have succeeded in DeFi development at an institutional scale are not the ones with the most sophisticated smart contracts. They are the ones that understood what the word “institutional” actually demands: accountability, auditability, and the kind of liquidity management in DeFi platforms that does not collapse under redemption pressure.

This piece is for product and strategy teams at the point of decision: whether to build, rebuild, or partner their way into a market that is real, growing, and unforgiving of shortcuts.

Why Institutional Capital Hesitates

The hesitation is not philosophical. Most institutional allocators have no ideological objection to decentralized finance. What they have is a fiduciary obligation. Before a pension fund, asset manager, or prime brokerage commits capital to any platform, it passes through a checklist that DeFi infrastructure, in its current state, routinely fails.

That checklist has three categories. First, regulatory compliance in DeFi platforms: does the platform meet KYC, AML, and sanctions screening requirements consistent with the allocator’s home jurisdiction? Second, counterparty risk: In the absence of a central intermediary, who is accountable when something goes wrong? Third, liquidity: can the platform handle large-ticket entry and exit without punishing price impact?

Most institutional DeFi platforms fail on at least two of the three. This is not a technology problem. It is an architectural problem that begins at the design phase.

“The gap between retail DeFi and institutional DeFi is not measured in smart contract sophistication. It is measured in legal certainty and exit reliability.”

Compliance Is the Product

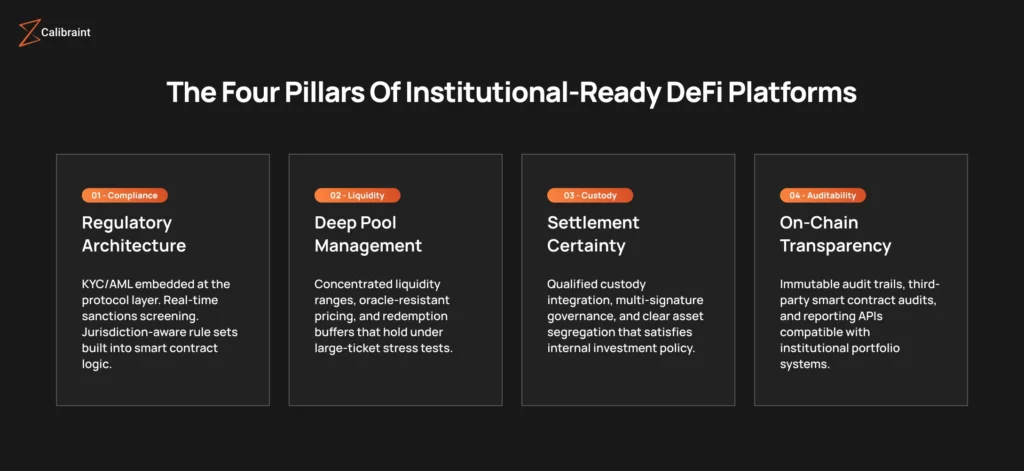

Regulatory compliance in DeFi platforms is not a feature bolted on after launch. In institutional contexts, it is the product. The distinction matters enormously for how teams should be structured, how budgets should be allocated, and how long timelines should be planned.

The DeFi legal framework for institutions varies significantly by jurisdiction, but several principles hold across markets. First, know-your-customer processes must be verifiable and auditable on demand.

Second, transaction monitoring cannot be an afterthought applied to outputs; it must be embedded in how the platform processes inputs. Third, wallet screening against OFAC, EU, and UN sanctions lists must run in real time, not on a weekly batch basis.

Platforms that treat compliance as a checkbox exercise discover the cost of that choice when the first institutional due diligence review arrives. The review does not ask whether the platform has a compliance officer. It asks whether the compliance architecture would survive a regulatory examination in three jurisdictions simultaneously.

The DeFi legal framework for institutions is also not static. MiCA in Europe, the evolving guidance from the SEC and CFTC in the United States, and Singapore’s MAS framework have each introduced obligations that touch custody, reporting, and classification. Building a platform without real regulatory counsel at the table is not a cost-saving measure. It is a liability.

Liquidity Is the Other Half of the Equation

Institutional liquidity in DeFi is a subject that receives considerably less attention than compliance and considerably more damage when it is handled poorly. A platform can pass every KYC screen and still be unusable for institutional purposes if the liquidity mechanics are not engineered for scale.

The problem is structural. Most decentralized exchange protocols were designed for retail order sizes. When a fund attempts to enter or exit a position of meaningful size, the price impact can be severe enough to erase the yield differential that made the trade attractive in the first place. Liquidity management in DeFi platforms that serve institutional capital requires a fundamentally different design philosophy.

Three specific mechanisms matter most. Concentrated liquidity ranges allow market makers to deploy capital more efficiently within defined price bands, reducing slippage for large trades. Oracle-resistant pricing mechanisms protect against manipulation that becomes more tempting as trade sizes grow. And redemption buffers, pre-funded reserve tranches that can absorb exit flows without triggering cascade liquidations, are increasingly non-negotiable for any platform that intends to hold significant institutional allocation.

The firms doing this well have also invested in institutional liquidity in DeFi through relationships. Market-making partnerships backed by strong balance sheets have often shown greater resilience in absorbing large order flows during periods of market stress. Research on liquidity provision also indicates that purely algorithmic market makers may reduce participation during volatility, which can amplify short-term liquidity gaps in stressed conditions.

The DeFi Legal Framework in Practice

Legal architecture is where many well-funded institutional DeFi platforms have stumbled. The DeFi legal framework for institutions is not merely about registering an entity in a favorable jurisdiction and hoping that the underlying protocol’s decentralization provides a liability shield. Regulators in most major markets have made clear that the substance of an activity, not its technical form, determines its classification.

This has practical implications. A platform that pools assets, provides yield, and allows redemption looks like an investment fund to a securities regulator, regardless of whether it runs on smart contracts. A platform that facilitates currency conversion looks like a money transmitter, regardless of whether the matching happens on-chain. The DeFi legal framework for institutions must therefore be built around what the platform actually does.

The platforms that have successfully attracted institutional capital have generally taken one of two approaches. Some have sought regulatory licensing directly, accepting the compliance costs and operational constraints in exchange for the clarity that a formal license provides. Others have built permissioned layers on top of permissionless protocols, creating a compliant access point for institutional participants while leaving the underlying protocol open. Both approaches work. The choice depends on the target market, the regulatory environment, and the team’s appetite for ongoing compliance investment.

What a Well-Structured Platform Actually Looks Like

A mid-sized asset manager allocating to a yield-generating DeFi protocol needs to satisfy its own compliance team, its custodian, and, in many cases, its auditor before the first dollar moves. What that process looks like in practice offers a useful lens on what institutional DeFi platforms need to deliver.

The compliance team expects to see documentation of how the platform screens wallets, how it handles flagged addresses, and what the escalation process is when a transaction triggers a monitoring alert. These processes must be described in language that maps to internal policy frameworks, not in blockchain terminology that requires translation.

The custodian needs to understand how assets are held during transit, how settlement finality is determined, and how the platform handles smart contract failures or governance exploits. These answers must be defined before the conversation begins, not discovered during integration discussions.

The auditor focuses on revenue recognition, fee structures, and how the platform’s on-chain activity maps to traditional accounting categories. A platform that cannot answer these questions has not been built for institutional capital, regardless of how sophisticated its protocol architecture may be.

Institutional liquidity in DeFi is, at its core, an operational confidence problem as much as a technical one. The platforms that close institutional mandates are the ones that have done the work of translating decentralized mechanics into the governance language that institutional counterparties already speak.

Teams building institutional DeFi platforms consistently underestimate the cost of the compliance and legal infrastructure relative to the protocol development itself. The technical work of building a secure, audited smart contract system is well-understood and priced in the market. The work of building a compliance architecture that satisfies multi-jurisdictional institutional requirements is less predictable and far more dependent on ongoing regulatory developments.

The second common error is treating liquidity management in DeFi platforms as a launch-day problem. In practice, liquidity architecture needs to be designed before the smart contracts are written, because the constraints it imposes affect every downstream technical decision. Retrofitting liquidity mechanics onto an existing protocol is expensive, slow, and often incomplete.

The third error is underestimating the sales cycle. Institutional capital allocation decisions involve multiple stakeholders, extended due diligence periods, and approval processes that can run for quarters. Platforms that have not anticipated this reality run out of runway before the first institutional commitment closes.

The Forward Position

The DeFi legal framework for institutions is starting to take clearer shape. Expectations around custody, reporting, and counterparty risk are becoming more defined.

Platforms that get this right early will have an advantage. Institutional allocation to DeFi has already started in a few markets and is gradually becoming part of broader portfolio discussions.

Building for institutional DeFi is a different kind of work. It involves more coordination, longer timelines, and a deeper understanding of how institutional participants evaluate risk and operations. At the same time, there is still room in the market for platforms that focus on getting the fundamentals right.

The question is not whether institutional capital will move into decentralized finance. That shift is already underway. What matters now is which platforms are actually prepared to support it properly.

1. How can DeFi platforms improve liquidity for institutional users?

DeFi platforms can improve liquidity by integrating with professional market makers, enabling deeper pools, and offering structured liquidity programs. Clear risk controls, reliable pricing mechanisms, and efficient execution also make participation easier for institutional users.

2. What is institutional liquidity in DeFi?

Institutional liquidity in DeFi refers to large-scale capital participation from regulated entities such as asset managers, funds, and financial firms. It is characterized by higher volume, stricter risk requirements, and expectations around transparency, custody, and compliance.

3. What are the biggest compliance challenges in DeFi for institutions?

The main challenges include meeting KYC and AML requirements, handling wallet-level risk screening, aligning with existing regulatory frameworks, and ensuring auditability of on-chain activity. Many platforms also struggle to present these processes in a way that fits institutional compliance standards.

4. What are the biggest liquidity risks in DeFi for institutions?

Key risks include low market depth during volatility, slippage on large trades, smart contract vulnerabilities, and the sudden withdrawal of liquidity providers. Fragmented liquidity across protocols can also make execution less predictable for large allocations.

Calibraint

Author

April 13, 2026

Let's Start A Conversation

Manage Consent

To provide the best experiences, we use technologies like cookies to store and/or access device information. Consenting to these technologies will allow us to process data such as browsing behavior or unique IDs on this site. Not consenting or withdrawing consent, may adversely affect certain features and functions.

Functional

Always active

The technical storage or access is strictly necessary for the legitimate purpose of enabling the use of a specific service explicitly requested by the subscriber or user, or for the sole purpose of carrying out the transmission of a communication over an electronic communications network.

Preferences

The technical storage or access is necessary for the legitimate purpose of storing preferences that are not requested by the subscriber or user.

Statistics

The technical storage or access that is used exclusively for statistical purposes.The technical storage or access that is used exclusively for anonymous statistical purposes. Without a subpoena, voluntary compliance on the part of your Internet Service Provider, or additional records from a third party, information stored or retrieved for this purpose alone cannot usually be used to identify you.

Marketing

The technical storage or access is required to create user profiles to send advertising, or to track the user on a website or across several websites for similar marketing purposes.