SWIFT and Chainlink CCIP Enable Multi-Bank Tokenized Bond Settlement, Accelerating RWA Adoption

Calibraint

Author

January 28, 2026

Last updated: March 2, 2026

The current financial infrastructure is a series of disconnected silos. For decades, the global banking system has operated on fragmented rails where a cross-border bond settlement feels more like a relay race than a digital transaction. The friction is palpable: multi-day settlement windows, manual reconciliation, and a heavy reliance on intermediaries that drain alpha.

You deserve a unified financial ecosystem. This guide explores the landmark 2026 shift where SWIFT successfully orchestrated a multi-bank tokenized bond settlement using Chainlink CCIP. We will detail how this integration solves the “digital island” problem and why 2026 marks the definitive year for RWA developmentwithin regulated frameworks.

From Fragmented Rails to Coordinated Infrastructure

For years, institutional blockchain initiatives suffered from a common flaw. Each bank built isolated ledgers that could not communicate beyond their own ecosystem. These environments replicated legacy inefficiencies while introducing new operational and reconciliation risks.

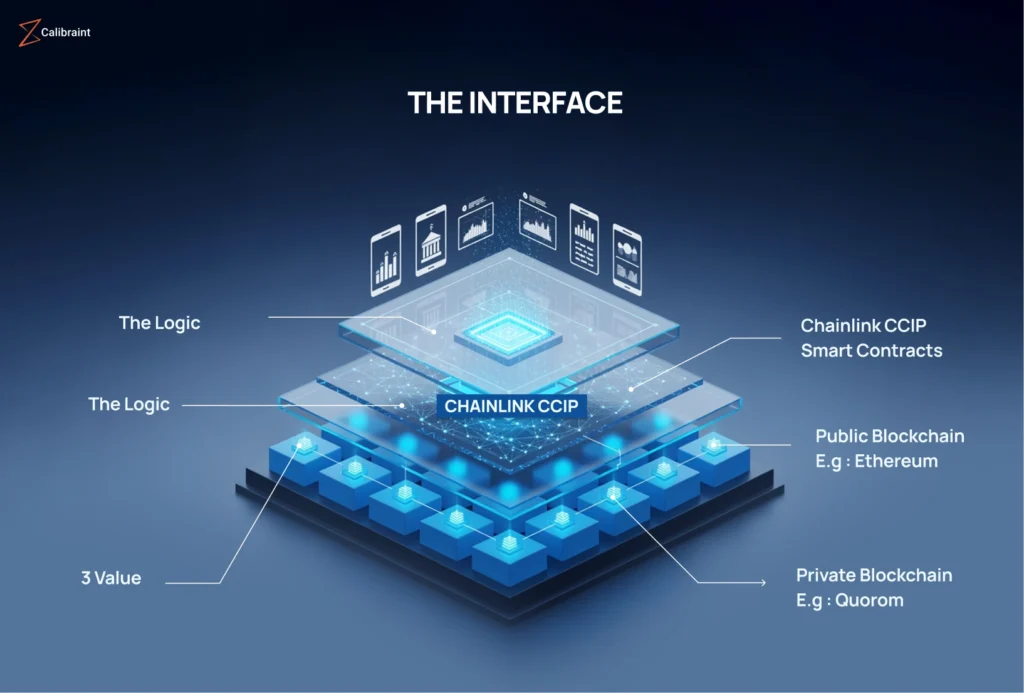

Rather than replacing existing infrastructure, SWIFT acts as the orchestration layer. Its ISO 20022 messaging standard provides a familiar control plane that institutions already trust. Chainlink CCIP operates beneath that layer, enabling secure, standardized cross-chain communication and synchronized asset movement across multiple blockchain environments.

This architecture allows banks to transact tokenized bonds without abandoning existing compliance models, custody frameworks, or settlement controls, resolving fragmentation at the infrastructure level rather than the asset level.

Institutional blockchain adoption is now transitioning from proof-of-concept validation to execution-oriented pilots. Since 2024, institutions including BNP Paribas, BNY Mellon, and Euroclear have participated in controlled initiatives exploring how blockchain networks can integrate with production financial infrastructure.

One notable initiative involves the Cross-Chain Interoperability Protocol developed by Chainlink in collaboration with SWIFT. These programs demonstrate how the SWIFT messaging network can function as a single access point to multiple blockchains, enabling tokenized asset settlement without requiring banks to redesign their back-office architecture.

While still governed by regulatory oversight and phased deployment, these initiatives signal a structural shift toward production-grade interoperability rather than isolated experimentation.

Solving the Fragmentation Crisis

Institutional crypto adoption stalled for years because of fragmentation. Every bank built its own private ledger, creating “digital islands” that could not communicate. This locked liquidity and increased operational risk.

Chainlink CCIP acts as the abstraction layer. It handles the technical complexity of cross-chain communication, allowing you to focus on the financial product rather than the underlying infrastructure. When a bank in London settles a tokenized bond with a counterparty in Singapore, CCIP ensures the message, the data, and the value move in a single, atomic transaction.

This eliminates the need for T+2 settlement. In this new paradigm, we move toward T+0. The bond and the payment swap simultaneously, removing counterparty risk and freeing up billions in dormant capital.

The Mechanics of Atomic Settlement

To understand why this matters for your bottom line, look at the Delivery vs. Payment (DvP) workflow. In legacy systems, this process involves multiple clearing houses and central securities depositories. In the 2026 multi-bank trial, the workflow looked vastly different.

Issuance: Manual legal and administrative workflows → Programmatic issuance

Settlement: T+2 with intermediary fees → T+0 atomic settlement

Liquidity: Limited secondary markets → 24/7 global trading access

The intelligence of this system lies in the smart contract. It governs the entire lifecycle of the asset. Interest payouts and redemptions happen automatically based on preset conditions. This reduces the need for a massive “paying agent” infrastructure, significantly lowering the total cost of ownership for debt instruments.

Quantifying the Business Impact

The move toward tokenized bonds is driven by a cold, hard look at the balance sheet. While initial implementation requires an upfront investment, the long-term ROI is undeniable.

Operational Phase

Legacy Cost Driver

2026 Tokenized Model

Issuance

Legal/Admin heavy

Programmatic issuance

Settlement

T+2 / Intermediary fees

T+0 / Atomic

Servicing

Manual coupon reconciliation

Automated Smart Contracts

Liquidity

Highly illiquid secondary market

24/7 global secondary trading

Lifecycle Automation as the Primary Value Driver

Settlement efficiency often gets the spotlight, but it is not where long-term value compounds.

The structural advantage of tokenized bonds emerges after issuance, when smart contracts govern the asset across its entire lifecycle. Coupon payments, interest calculations, and principal redemptions execute automatically based on predefined terms embedded at issuance.

This automation reduces reliance on traditional paying agents and removes layers of manual reconciliation that persist across legacy bond servicing.

For issuers and investors, lifecycle automation delivers measurable outcomes:

Lower ongoing servicing and administrative costs

Fewer operational errors across payment and reporting cycles

Fully auditable and transparent cash flow execution

Continuous access to secondary market liquidity without manual intervention

In institutional environments, these efficiencies matter more than marginal settlement speed gains. They reshape how debt instruments are managed, reported, and scaled across portfolios.

Strategic Roadmap for Executives

If you are a product head or a strategic thinker, your goal is to avoid being left behind on legacy rails. The migration to on-chain finance is an “internet moment” for capital markets.

Audit Your Messaging: Ensure your systems are fully ISO 20022 compliant. This is the prerequisite for interacting with the SWIFT-ledger.

Select Interoperability Standards: Don’t lock yourself into a single blockchain. Use an abstraction layer like CCIP to maintain optionality.

Focus on Lifecycle Automation: The value is not just in the token, but in the automated servicing of that token.

Tokenized Bonds Are Becoming Institutional Infrastructure

As tokenized bonds move toward production-grade settlement, success depends on more than infrastructure. It requires partners who understand institutional constraints, regulatory expectations, and real-world operating models.

Calibraint brings deep experience in RWA development, blockchain integration, and enterprise-grade delivery. We work with financial institutions to design tokenized bond systems that align with governance requirements, integrate seamlessly with existing infrastructure, and scale without unnecessary risk.

If you are evaluating how tokenized bonds, SWIFT blockchain integration, or Chainlink CCIP fit into your institutional roadmap, we can help you move from concept to execution with clarity and confidence.

FAQs

1. How does Chainlink CCIP enable tokenized bond settlement between banks?

Chainlink CCIP enables tokenized bond settlement by securely connecting different blockchain networks used by banks and synchronizing asset and payment transfers across them. When SWIFT initiates a settlement instruction using ISO 20022 messaging, CCIP validates the instruction and ensures that the tokenized bond and the corresponding payment settle simultaneously, supporting atomic delivery versus payment without relying on multiple intermediaries or manual reconciliation.

2. Why is SWIFT’s multi-bank tokenized bond settlement a game-changer for RWA adoption in 2026?

SWIFT’s multi-bank tokenized bond settlement is a turning point because it integrates blockchain-based assets into the existing global financial infrastructure instead of operating alongside it. By using trusted messaging standards and established compliance frameworks, SWIFT enables regulated institutions to adopt real world asset tokenization at scale, marking the transition from limited pilots to production-ready capital markets infrastructure in 2026.

3. What does SWIFT’s tokenized bond settlement mean for investors and the broader crypto market?

For investors, tokenized bond settlement improves transparency, reduces counterparty risk, and enables faster access to global fixed-income products through automated settlement and lifecycle management. For the broader crypto market, it reinforces blockchain’s role as institutional financial infrastructure and positions real world asset tokenization as a stable, regulated growth driver rather than a speculative use case.

Calibraint

Author

January 28, 2026

Last updated: March 2, 2026

0

Let's Start A Conversation

Manage Consent

To provide the best experiences, we use technologies like cookies to store and/or access device information. Consenting to these technologies will allow us to process data such as browsing behavior or unique IDs on this site. Not consenting or withdrawing consent, may adversely affect certain features and functions.

Functional

Always active

The technical storage or access is strictly necessary for the legitimate purpose of enabling the use of a specific service explicitly requested by the subscriber or user, or for the sole purpose of carrying out the transmission of a communication over an electronic communications network.

Preferences

The technical storage or access is necessary for the legitimate purpose of storing preferences that are not requested by the subscriber or user.

Statistics

The technical storage or access that is used exclusively for statistical purposes.The technical storage or access that is used exclusively for anonymous statistical purposes. Without a subpoena, voluntary compliance on the part of your Internet Service Provider, or additional records from a third party, information stored or retrieved for this purpose alone cannot usually be used to identify you.

Marketing

The technical storage or access is required to create user profiles to send advertising, or to track the user on a website or across several websites for similar marketing purposes.