Tokenized RWAs : Reliable Yields in Crypto Volatility Guide to Stable Returns & Maturity

Calibraint

Author

March 13, 2026

Digital asset markets reward conviction, yet they often test patience. Price cycles move quickly, liquidity shifts overnight, and the search for dependable yield continues to challenge investors across the ecosystem. Over the past few years, a clear pattern has emerged. Capital that once chased speculative returns now seeks instruments with predictable income and measurable maturity structures.

This shift explains the growing attention toward tokenized RWAs for stable crypto yields. Real-world assets brought onto blockchain infrastructure introduce an entirely different yield foundation. Instead of relying on token incentives or volatile liquidity pools, these instruments draw income from assets such as government bonds, credit facilities, and structured debt products.

The transition also highlights a new category of infrastructure work inside the digital asset economy. Sophisticated RWA development frameworks now connect traditional financial instruments with programmable blockchain environments. This intersection allows digital asset platforms to distribute income streams that originate from established financial markets.

This guide explains how tokenized RWAs for stable crypto yields function, why maturity structures matter, and how yield-bearing blockchain assets are gradually becoming an anchor during periods of crypto volatility.

When Crypto Yield Lost Its Predictability

The early phase of decentralized finance introduced a wave of high-return opportunities. Liquidity mining programs, algorithmic stablecoins, and token incentives promised rapid gains. For a period, the model attracted enormous capital.

Then the system revealed its weaknesses.

The collapse of Terra Luna exposed the fragility of algorithmic yield structures. Liquidity pools that once appeared sustainable quickly unraveled when market confidence disappeared. Several lending platforms followed similar paths as collateral values dropped.

Markets do not reward yield that lacks a real economic source.

This realization pushed investors toward a different idea. Instead of generating returns through token emissions, yield could originate from real assets that already produce income in traditional financial systems.

That concept sits at the center of Tokenized RWAs for Stable Crypto Yields.

At the most practical level, tokenized Treasuries are on-chain representations of short-duration government debt. When you hold a token in one of these products, you hold a claim on the underlying securities held by a qualified custodian. Yield accrues daily, settlement happens on-chain, and redemptions are processed far faster than traditional fund mechanics allow.

The yield profile tracks the federal funds rate. In the current environment, that has meant short-duration government securities yielding in the range of 4.5 to 5.2 percent annually, with minimal credit risk. For a crypto-native treasury function, that is a meaningful return on capital that would otherwise sit in a zero-yield stablecoin.

Three products have established credible track records worth studying:

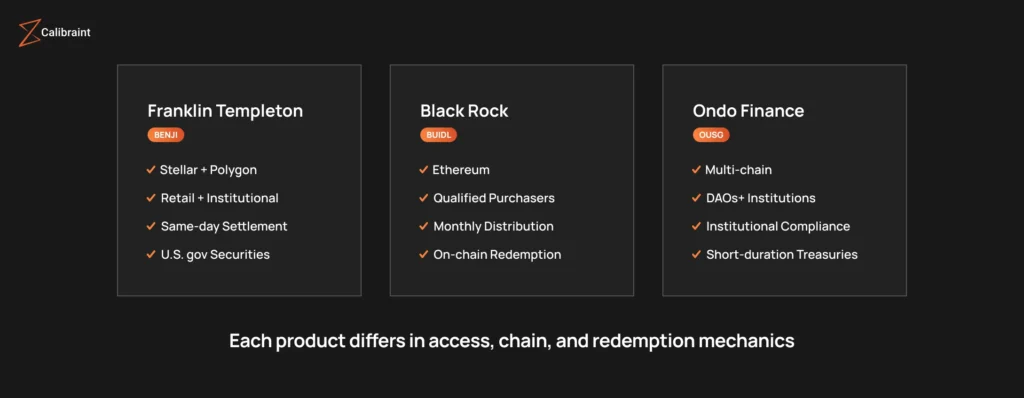

Franklin Templeton’s BENJI operates on Stellar and Polygon, offering retail and institutional access to a tokenized government money market fund. The underlying portfolio holds U.S. government securities with same-day settlement.

BlackRock’s BUIDL, built on Ethereum in partnership with Securitize, functions as a tokenized Treasury product accessible to qualified purchasers. It generates yield daily and distributes monthly, with redemptions settled on-chain.

Ondo Finance’s OUSG offers exposure to short-duration U.S. Treasuries with institutional-grade compliance built in, and has gained significant traction among DAOs and crypto-native treasuries looking to put idle capital to work.

Each product differs in jurisdiction, access requirements, redemption mechanics, and yield distribution. The due diligence required to evaluate them is the same you would apply to any structured product.

The Maturity Question: What “RWA Token Maturity” Actually Means

One concept that deserves more careful treatment is maturity structure in tokenized RWAs. Unlike a single fixed-income bond with a defined duration, most tokenized RWA products hold rolling portfolios of short-duration instruments. This creates a continuously renewing yield exposure rather than a fixed payoff date.

Understanding this distinction matters for portfolio planning. A tokenized Treasury product holding 30 to 90-day bills will reset its yield more frequently than one holding 6 to 12-month notes. In a falling-rate environment, shorter duration means faster yield compression. In a rising rate environment, it means faster capture of higher rates.

For portfolios hedging crypto volatility, shorter-duration tokenized RWA products generally offer better liquidity and faster repositioning. For portfolios seeking yield optimization over a defined horizon, products with slightly longer weighted average maturity may offer better carry.

The right structure depends on what you are hedging against: correlation risk, liquidity risk, or opportunity cost.

Private Credit and Yield-Bearing Tokenized Assets Beyond Treasuries

Tokenized Treasuries represent the most liquid and regulated entry point into tokenized RWAs. But the broader yield-bearing tokenized asset space extends into private credit, real estate debt, and trade finance.

Centrifuge, one of the earlier platforms in this space, has facilitated over $500 million in real-world loan origination through tokenized asset pools. Borrowers in sectors like trade receivables and commercial real estate access capital through on-chain structures, and token holders earn yield that reflects the credit risk of those pools.

Maple Finance has similarly moved toward institutional borrowers with verifiable track records, offering fixed-income-like products that target higher yields with defined risk parameters.

These yield-bearing tokenized assets carry more credit risk than government securities. The yield premium is real. So is the underwriting requirement. Any serious allocation to this category requires the same credit analysis discipline you would apply to private debt fund selection.

The interesting development is that RWA development infrastructure now supports that analysis at scale. Credit dashboards, on-chain repayment histories, and audited reserve attestations are becoming table stakes for credible platforms.

Hedging Crypto Volatility with RWAs: The Portfolio Logic

Hedging crypto volatility with RWAs is less about eliminating risk and more about introducing structural diversification that does not move with crypto sentiment.

The correlation argument is straightforward. During the crypto market drawdowns of 2022 and early 2023, stablecoins held parity but generated no yield. DeFi products collapsed in value alongside the broader market. Tokenized Treasuries, had they been available at the scale they are today, would have continued accruing yield throughout, entirely disconnected from crypto price action.

For a portfolio carrying meaningful crypto exposure, allocating a portion to tokenized RWAs functions as a liquidity buffer with yield. It does not hedge price risk in the traditional derivative sense. What it does is ensure that a portion of the portfolio continues compounding regardless of market conditions.

Institutional treasuries managing crypto holdings have begun formalizing this approach. Several publicly known DAOs, including MakerDAO and Frax Finance, have allocated significant portions of their reserves to tokenized government securities precisely because the yield and stability profile serve their operational needs better than holding pure stablecoin exposure.

What Separates a Serious Platform from a Marketing Exercise

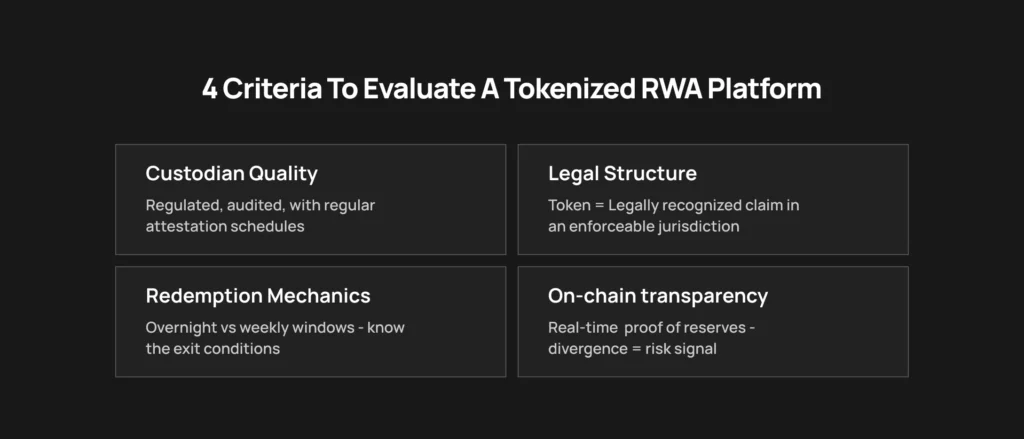

Not all tokenized RWA products are equal. The following criteria distinguish platforms with genuine infrastructure from those riding the narrative:

Custodian quality matters first. The underlying asset must sit with a regulated, audited custodian. Attestations should be available on a regular schedule, not quarterly PDFs buried in a website.

Legal structure matters second. The token must represent a legally recognized claim on the underlying asset in a jurisdiction with clear enforcement. Structures built on ambiguous legal opinions introduce redemption risk that is not reflected in the yield.

Redemption mechanics matter third. Knowing under what conditions redemptions are honored, and at what speed, is essential. Products with overnight or same-day redemption mechanics function very differently from those with weekly or monthly windows.

On-chain transparency matters fourth. Any serious tokenized RWA product should offer verifiable, real-time, or near-real-time proof of reserves. If the on-chain data and the custodian attestation diverge, that is a risk signal.

Tokenized RWAs are not a temporary product category waiting to be disrupted. They represent the early infrastructure layer of a much larger shift in how fixed-income and credit products are originated, distributed, and held.

The next phase of RWA development will involve secondary market liquidity, cross-chain composability, and integration into broader DeFi yield strategies. Products that today sit in isolated silos will become components of programmable portfolios, automatically rebalancing between yield-bearing tokenized assets based on rate conditions and risk parameters.

That infrastructure is being built right now. The institutions building it are responding to demonstrated demand from capital allocators who want stable, verifiable, yield-generating positions that fit within their existing compliance and reporting frameworks.

A Final Word: The Cost of Waiting

Markets reward those who recognize structural shifts early. Tokenized RWAs have moved beyond experimentation and entered real financial infrastructure. The focus now turns to portfolio architecture and disciplined risk management.

Platforms with strong infrastructure, transparent reserve practices, and clear legal structures are already setting the standard. Careful evaluation today allows investors to position capital before wider allocation pressure accelerates adoption.

Organizations ready to move from observation to execution benefit from working with experienced builders in this space. Calibraint supports financial institutions, crypto-native treasuries, and asset managers in designing compliant, yield-generating tokenized RWA solutions through advanced enterprise blockchain and RWA development expertise.

FAQs

1. How can tokenized RWAs provide stable crypto yields during market volatility?

Tokenized real-world assets generate income from traditional financial instruments such as government bonds or credit facilities. Because the yield comes from these underlying assets rather than crypto market activity, returns remain more stable even when digital asset prices fluctuate.

2. What are the best tokenized treasuries for stable yields in 2026?

Several well-known products offer tokenized exposure to government securities. Examples include BENJI from Franklin Templeton, BUIDL from BlackRock, and OUSG from Ondo Finance. Each product differs in access requirements, compliance structure, and redemption mechanics.

3. How does maturity work in tokenized RWAs for stable returns?

Most tokenized RWA products hold short-duration financial instruments such as treasury bills. These instruments mature periodically, and the portfolio reinvests them to maintain continuous yield exposure. The maturity cycle determines how often the yield rate adjusts.

4. Can yield-bearing tokenized assets help hedge crypto volatility effectively?

Yield-bearing tokenized assets can provide portfolio balance by generating income from traditional financial markets. While they do not eliminate crypto price risk, they add a stable return component that continues earning yield during volatile market periods.

5. What guide should Web3 users follow for stable yields from tokenized RWAs?

Web3 users should evaluate the quality of the underlying assets, the credibility of the custodian, the legal ownership structure, and the redemption conditions. Reviewing reserve transparency and maturity structures helps ensure the tokenized RWA product supports reliable yield generation.

Calibraint

Author

March 13, 2026

Let's Start A Conversation

Manage Consent

To provide the best experiences, we use technologies like cookies to store and/or access device information. Consenting to these technologies will allow us to process data such as browsing behavior or unique IDs on this site. Not consenting or withdrawing consent, may adversely affect certain features and functions.

Functional

Always active

The technical storage or access is strictly necessary for the legitimate purpose of enabling the use of a specific service explicitly requested by the subscriber or user, or for the sole purpose of carrying out the transmission of a communication over an electronic communications network.

Preferences

The technical storage or access is necessary for the legitimate purpose of storing preferences that are not requested by the subscriber or user.

Statistics

The technical storage or access that is used exclusively for statistical purposes.The technical storage or access that is used exclusively for anonymous statistical purposes. Without a subpoena, voluntary compliance on the part of your Internet Service Provider, or additional records from a third party, information stored or retrieved for this purpose alone cannot usually be used to identify you.

Marketing

The technical storage or access is required to create user profiles to send advertising, or to track the user on a website or across several websites for similar marketing purposes.