How AI Is Transforming Fraud Detection and Risk Management in FinTech

Calibraint

Author

March 5, 2026

You already know the threat is real. Each week brings a new headline: a payment processor breached, a bank’s customers targeted, or a synthetic identity bypassing multiple checks. Many institutions are discovering that traditional approaches cannot address modern financial crime.

AI development underpins the systems that keep modern financial institutions secure. AI driven fraud detection in FinTech is now a core expectation for organizations that aim to safeguard both their customers and their business performance.

This article explores how that shift is happening, what the technology achieves beneath the surface, and why early adopters gain lasting operational and strategic advantages.

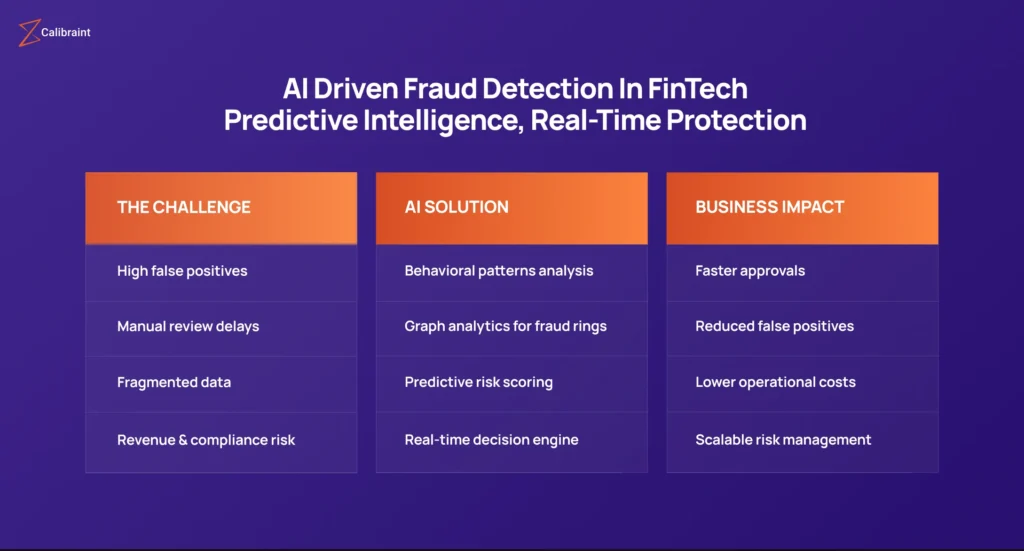

Static Controls in a Dynamic Threat Economy

Traditional fraud prevention was built on a simple premise. Write a rule for every threat you have already seen. Flag transactions over a certain amount. Block cards are used in two countries within an hour. Decline anything that does not match the usual pattern.

For a long time, that worked. Fraud moved at a human pace. Today, it does not.

Criminals now operate automated platforms that probe millions of accounts simultaneously. They use deepfake voice technology to defeat call center verification. They build synthetic identities, fake people with real credit histories, that take years to surface as fraudulent. Against that level of sophistication, a static ruleset is not a defense. It is a liability.

The second cost is invisible until you look at your churn numbers. Every time a legitimate customer gets blocked during a perfectly normal transaction, they feel the friction. A declined card at a hotel. A frozen account during an overseas trip. A flagged payment for a large but completely routine purchase. That friction drives customers toward competitors who get it right.

Real time fraud prevention must now solve two problems at once: catch the threat and protect the experience. Legacy systems were never designed to do both.

The Structural Advantage of Learning Systems

The distinction between a rule engine and an AI model lies in adaptability. A rules engine recognizes only what it has been programmed to detect. AI models learn patterns continuously and identify anomalies that have no precedent.

AI driven fraud detection in FinTech operates on two layers:

Supervised Learning: Trains on historical fraud cases, known tactics, and documented patterns to recognize high-probability fraudulent behavior.

Behavioral analytics enhances this capability. It is not just transaction amounts and locations. Systems monitor device usage, navigation habits, typing rhythms, and interaction flows. Fraudsters may replicate credentials, but they cannot replicate years of behavioral history.

Passive Security in Practice

Behavioral intelligence underpins what practitioners call passive security: authentication and risk assessment happening invisibly, without interrupting the customer. The most effective AI driven fraud detection in FinTech works quietly, protecting legitimate transactions while targeting suspicious behavior.

Consumer fraud losses continue to rise. According to the Federal Trade Commission, fraud across digital channels has increased sharply in recent years, emphasizing the need for stronger detection mechanisms.

The Nilson Report projects sustained growth in global card fraud as digital payments scale.

Research from Gartner and McKinsey & Company highlights that financial institutions are prioritizing AI in finance for fraud detection and risk intelligence. Institutions integrating these systems report measurable improvements in detection accuracy while reducing operational overhead.

Major payment networks, including Mastercard and Visa, publicly emphasize AI-driven fraud intelligence as core infrastructure for protecting transactions.

How AI Driven Fraud Detection in FinTech Works

AI integrates multiple layers of intelligence:

Data Inputs

Transaction history

Device fingerprints

Behavioral biometrics

Network relationships

Location patterns

AI Risk Layer

AI fraud detection models

Graph network mapping of accounts

Predictive risk AI finance scoring

Anomaly detection systems

Decision Layer

Real-time transaction scoring

Automated approvals

Escalation to human review when necessary

Continuous Learning

Human feedback loop

Model refinement

Audit and explainability logs

The ROI That Does Not Show Up on the Fraud Report

Most discussions about preventing financial fraud emphasize avoiding direct losses: the money that isn’t stolen. That is real, and it matters. But the deeper ROI of risk management in banking built on AI shows up in places that do not appear on the fraud report.

First, there is operational efficiency. AI fraud detection eliminates up to 80% of manual review volume. That shifts your analyst team from triaging hundreds of low-confidence alerts, most of which are legitimate, to investigating the high-confidence cases that actually require human judgment. You get better outcomes with fewer resources.

Second, and increasingly important: security is now a brand signal. A platform known for seamless, intelligent protection attracts a different caliber of user. Institutional clients run vendor risk assessments that now include AI security posture. Retail customers choose banks that do not make them feel like suspects. The quality of your FinTech risk management infrastructure directly influences who chooses to bank with you.

Third is regulatory positioning. The compliance cost of a fraud event, fines, audits, and remediation dwarfs the cost of preventative AI infrastructure. Institutions that demonstrate sophisticated, explainable AI driven fraud prevention systems are building relationships with regulators based on transparency rather than damage control.

The technology is only as good as the data feeding it. Every successful deployment of AI driven fraud detection in FinTech starts with the same foundational work: unifying the data environment.

Most institutions enter this process with their information scattered across separate systems. Transaction history in one place, device intelligence in another, customer support interactions somewhere else entirely. That fragmentation is itself a security vulnerability, because the signals that indicate fraud often sit across those silos simultaneously. A transaction that looks fine in isolation looks deeply suspicious when you can see the device behavior and the recent support call in the same view.

Once the data foundation is clean and unified, the model can be trained with the specificity your transaction environment requires. Generic models exist, but the institutions seeing the strongest results are those that train on their own fraud history, their specific customer base, their typical transaction patterns, and their particular risk profile.

The Open Loop: Human Intelligence Feeding the Machine

The most important ongoing practice is what practitioners call the Open Loop, a structured feedback process where human investigators review confirmed fraud cases and feed those findings back into the model. Every confirmed case is a lesson. Every edge case that the system missed becomes training data for the next version.

This creates a compounding advantage. The longer the system runs with disciplined feedback, the more precisely it is calibrated to your specific threat environment. Institutions that built this feedback loop three years ago are running models that are materially more accurate than anything a new deployment can match on day one.

Where to Start When Evaluating AI Driven Fraud Detection

Most institutions no longer question whether to adopt AI driven fraud detection in FinTech. The real challenge is knowing how to begin and how to implement it without disrupting ongoing operations.

The first step is data. Before selecting a model or vendor, you need a clear view of your data environment: what information is collected, where it resides, how accurate it is, and how it can be consolidated into a unified, usable stream. This audit usually takes weeks, not months, but it sets the foundation for everything that follows.

The second step is organization and workflow. AI driven fraud prevention does not replace your fraud team. Instead, it changes how the team works. Analysts who previously reviewed routine alerts now focus on providing feedback that trains and improves the AI system. This requires careful change management, not just technology deployment.

Institutions that treat AI as simply a software purchase often see limited results. Those that approach it as a transformation of their operating model, using technology to enhance human expertise, are the ones that gain a lasting advantage.

See What Your Risk Framework Is Missing

Financial organizations do not fail due to a lack of expertise. The challenge lies in infrastructure designed for a slower, less complex era of fraud. Modern AI driven fraud detection in FinTech requires systems built around your specific transaction patterns, customer behavior, and risk profile.

At Calibraint, we help financial institutions close that gap with AI systems built around your transaction.

We help financial institutions implement fraud detection architectures that reduce false positives, identify threats earlier, and scale seamlessly without impacting the customer experience.

A structured assessment can reveal gaps in your current setup and highlight where AI driven fraud detection delivers the greatest operational and strategic impact. For a practical, no-pressure conversation about what is possible for your organization, visit https://www.calibraint.com/contact

FAQs

1. How is AI transforming fraud detection in FinTech?

AI driven fraud detection in FinTech identifies suspicious transactions in real time, learns from new fraud patterns, and reduces false positives, improving both security and customer experience.

2. What role does AI play in FinTech risk management?

AI supports FinTech risk management by analyzing transaction data, predicting potential threats, and providing actionable insights to prevent financial losses and operational inefficiencies.

3. What are real-world examples of AI fraud prevention in FinTech?

Major payment networks and digital banks use AI to monitor behavioral patterns, flag anomalous activity, and automate risk scoring, reducing fraud while keeping customer friction minimal.

Calibraint

Author

March 5, 2026

Let's Start A Conversation

Manage Consent

To provide the best experiences, we use technologies like cookies to store and/or access device information. Consenting to these technologies will allow us to process data such as browsing behavior or unique IDs on this site. Not consenting or withdrawing consent, may adversely affect certain features and functions.

Functional

Always active

The technical storage or access is strictly necessary for the legitimate purpose of enabling the use of a specific service explicitly requested by the subscriber or user, or for the sole purpose of carrying out the transmission of a communication over an electronic communications network.

Preferences

The technical storage or access is necessary for the legitimate purpose of storing preferences that are not requested by the subscriber or user.

Statistics

The technical storage or access that is used exclusively for statistical purposes.The technical storage or access that is used exclusively for anonymous statistical purposes. Without a subpoena, voluntary compliance on the part of your Internet Service Provider, or additional records from a third party, information stored or retrieved for this purpose alone cannot usually be used to identify you.

Marketing

The technical storage or access is required to create user profiles to send advertising, or to track the user on a website or across several websites for similar marketing purposes.